")

ju white

investment thesis

Microsoft (NASDAQ:MSFT) A strategic bet with the development and integration of Copilot, an AI-driven platform, put the company in a good position to drive quarterly conference calls and future business.

Launched in late 2022, Microsoft Copilot quickly became a key tool within the Microsoft suite, both for software engineers (via GitHub) and for non-coding tasks.

I think recent analysis shows that the market for Copilot is huge. Some forecasts suggest the tool could help Microsoft generate around $10 billion in annual revenue by 2026, assuming an 18% adoption rate among targeted users. (Please note that this tool was not released until November 1st last year). So to reach $10 billion in revenue in just three short years is incredible.

I think this shows that the potential earnings are: The scale Microsoft is thinking about: What they’re actually aiming for is a scale of The goal is to deploy AI tools across multiple sectors and industries.

Although I haven’t written since the winter before its fiscal second quarter earnings report, I remain bullish on Microsoft and see Copilot and its broader AI strategy as core to its growth. Masu. I believe Microsoft stock is a strong buy heading into the call on the 25th.

Why I do follow-up interviews

In January, I wrote about Microsoft’s work in gaming and how it’s underappreciated. I believe Copilot (albeit much more widely known) offers similar benefits to companies and incredible productivity gains to users.

Third quarter results are expected to be released after the bell on April 25th. With this, I will discuss (before the quarterly report) how his Copilot continues to improve and why this quarter will be key to the bottom line of his Copilot’s story. I wanted to do a follow-up that shows.

Microsoft’s latest enhancements to Copilot not only help users code simple functions using GitHub or create better research within Microsoft Word, but also improve enterprise productivity. is poised to redefine.

Recent major updates include automation of routine tasks such as sending and tracking invoices, as well as advanced coding features that allow developers to automatically refactor and optimize code within their applications. I am. I believe these advances are designed to significantly streamline operations, and not just in the world of Microsoft Office. These are automations that can impact departments such as accounting, which are likely using Microsoft Excel but are currently using other software to track and send invoices ( (think Quickbooks, which is not a Microsoft product).

To me, these new features are part of Microsoft’s broader strategy to build more sophisticated AI-driven capabilities into its suite of products. I think the hope is that this will make the company-wide Build developer conference in May the platform to announce these features (and more).

Co-pilot background

Introduced on September 21st of last year, Copilot quickly became a core feature for enterprise users with over 300 seats when it launched in November (November 1st).

The robust adoption of this tool reflects strong demand and perceived value among larger organizations (as we have deployed it to companies with more than 300 seats). I think small and medium-sized businesses will benefit tremendously as well, but their usage has not yet exploded to the same extent as for large enterprises.

Piper Sandler analysts predict that Copilot could generate approximately $10 billion in revenue by 2026, assuming an 18% adoption rate among qualified users.

I even think this prediction may indeed be conservative given Copilot’s integration across Microsoft’s broader software ecosystem (in addition to small and medium-sized business and individual adoption, we’re still seeing real-world adoption). Is not).

For example, Copilot helps automate tasks ranging from data analysis to content generation directly within user workflows in Microsoft 365. Small businesses can’t afford to hire data entry analysts or copy editors. AI will bring them great advances.

The tool costs $30 per user per month, so I think Microsoft has tailored Copilot’s features at a price point that most users can afford, especially when you consider the productivity gains.

Our enthusiasm for Copilot is reflected in our customer research. Jefferies analysts noted that thousands of organizations are awaiting its general availability.

When the tool was released in November, Microsoft had only two-thirds of a quarter to start shipping it to customers. Given that he had 13 weeks to get this tool into the hands of users, it’s interesting to see how this tool performed in the third quarter of the fiscal year (normal first quarter). I’m really looking forward to it.

Fiscal Q3 Forecasts

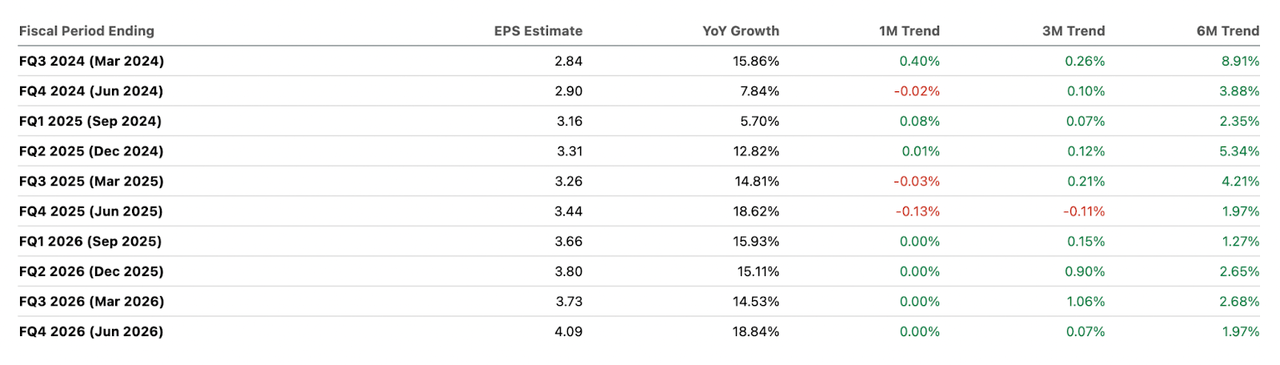

We admit that expectations for the upcoming fiscal third quarter earnings are quite high due to upward revisions to EPS estimates by sell-side analysts. If Microsoft hits these numbers (thanks in part to Copilot), EPS estimates suggest a significant performance improvement.

Analysts are predicting consensus EPS (earnings per share) of $2.84, which would represent solid year-over-year growth of approximately 15.86%. With this, revenue forecasts are solid, with consensus estimates projecting revenue to reach $60.85 billion, reflecting 15.12% year-over-year growth.

What I’m looking for on my phone

For me, I started with the last earnings release to set expectations for this one. Copilot was a big part of the story during the last earnings call, featured 52 times.

Last quarter, the company announced strong evidence of rapid adoption of Copilot.

GitHub’s revenue accelerated over 40% year-over-year due to growth across the platform and adoption of GitHub Copilot, the world’s most widely deployed AI developer tool. Currently, he has over 1.3 million paid GitHub Copilot subscribers, up 30% QoQ – FY Q2 Call

In addition to this, the enterprise adoption we saw in the fourth quarter was strong.

[Copilot] Already used by more than 10,000 organizations, including An Post, Holland America, and PG&E. – Recruitment for 2nd quarter of 2024

Therefore, for me it is mandatory to see how these numbers have been updated since my last call. I’m going to focus on use cases, how people are leveraging these powerful tools, rather than whether mentions of Copilot have increased since last quarter. The last call administrator briefly mentioned how Copilot is “scaling.” [its] Copilot also integrates with third-party systems to enable TAM. ” I’m going to pay close attention to how they’re doing this. I already know Copilot is used in places like invoice tracking, but qualitative data like this is essential to me. .

This makes me particularly interested in getting hard numbers related to Copilot’s adoption (as well as last quarter’s performance). For me, this includes the number of his Copilot seats or licenses sold, which gives a clearer picture of market penetration.

An added bonus is if management reveals the actual revenue (quarter-end occupancy) they receive from Copilot. I think this number may shock some analysts. For example, we already know that he has 1.3 million GitHub Copilot subscribers. At an average monthly cost of $18/month (Enterprise costs even higher at $39/month per seat), his ARR from Copilot is already over $250 million per year. I think his estimate of $10 billion in revenue by 2026 is quite possible. They may be conservative. These results are more skewed than the enterprise cost per seat and do not include Microsoft Office Copilot functionality.

evaluation

Microsoft stock currently trades at a 30% premium to its sector, but I believe this premium is justified with gross margins approximately 49% above the sector median. The company’s current non-GAAP forward P/E ratio is 35.33x and the sector median is 27.02x. The company’s current gross profit margin is an impressive 69.81%, far higher than the sector median of 48.95%.

While the forward P/E ratio may seem high, especially considering the high interest rate environment we live in, investors are wondering what Copilot can expect going forward, given the strong growth it has seen to date. I really think we need to pay attention to what’s going on. . I think Copilot will perform better than I expected.

If the company outperforms this earnings season, especially if its future P/E ratio is 45% to 50% above the current 30% premium over the sector median, the stock price could rise by 10% to reflect Microsoft’s strong performance. We expect it to rise by 15%. Product provision.

Comparison with my previous revenue forecast

When I wrote about Microsoft’s gaming division in January, I said that given the completed deal with Activision, Microsoft’s gaming division could boost the company’s market cap by as much as about 14% if it gains further industry penetration. We discussed the possibilities. In the last earnings call, management stated that “Activision contributed approximately 4 percentage points to revenue growth…”

Since then, the stock price has increased about 4%. I think there is strong upside potential for the stock, including a potential 10-15% share price increase from CoPilot. However, I am combining the remaining upside potential from the game (10% upside) with the potential Copilot upside that seems available. I think this makes my upside prediction conservative given that it gives the stock multiple catalysts/vehicles available to push the stock price higher.

Risks that affect profits

The biggest risk for me going into financial results announcements is expectations. Expectations are pretty high for Microsoft this quarter, given the notable analyst revisions over the past six months.

Analysts have increased their EPS estimates for this period by 8.91%. This reflects strong optimism regarding Microsoft’s performance, particularly in areas such as AI with products such as his Copilot. These are the highest upward revisions analysts have given in any quarter over the next three fiscal years (including the current fiscal year).

Microsoft’s Earnings Forecast Revised (Alpha Request Now)

While these positive revisions raise expectations, they also clearly come with risks. If Microsoft fails to live up to the expectations raised, especially in relation to his Copilot, the revaluation of the company’s stock could be downgraded.

But I’m optimistic and don’t think that will happen. The long-term outlook remains positive, driven by the transformative potential of what Copilot can do for people in industries from programming to accounting. These are real areas that are expected to drive future growth and efficiency.

conclusion

Ahead of Microsoft’s third quarter results, all eyes are on Copilot, the company’s flagship AI tool. Copilot is further expected to redefine productivity for enterprises. This earnings report is very important as it reveals the extent of Copilot’s integration and contribution to Microsoft’s revenue. Analysts remain optimistic, with AI capabilities driving significant growth, with Copilot predicting it could deliver around $10 billion in revenue by 2026.

I think high expectations, supported by a strong 8.91% EPS estimate increase over the past six months, indicate strong market confidence in Microsoft’s AI strategy, rather than undue optimism. Masu. Overall, I think the stock remains a strong buy. I’m looking forward to seeing what Microsoft will report.